- Slug: BC-CNS-Married Motorists,680

- Photos available (thumbnails, captions below)

By AUBREY RUMORE

Cronkite News

WASHINGTON – Single, widowed and divorced drivers in Phoenix are likely to pay higher insurance rates than married drivers with identical driving records, according to a recent report from the Consumer Federation of America.

Phoenix was one of 10 large cities across the U.S. where the federation sought quotes for a 30-year-old woman with a perfect driving record – but different family particulars. In all 10 cities, most rates were higher for that hypothetical customer if she was single, divorced, widowed or single with a child, the study showed.

Critics say that’s the wrong thing for insurers to focus on.

Buying auto insurance “shouldn’t remind people to go get married,” said J. Robert Hunter, director of insurance for the Consumer Federation of America. “Insurance pricing should remind people to be safe.”

But where consumer groups see rating criteria that have little to do with risk, others see a “sign of a healthy marketplace,” where different insurers are offering a range of pricing options.

Andrew Carlson, the legislative liaison for the Arizona Department of Insurance, said “there is nothing preventing” consumers from choosing a different insurance company.

“Consumers are free if they can find a better rate or premium,” Carlson added.

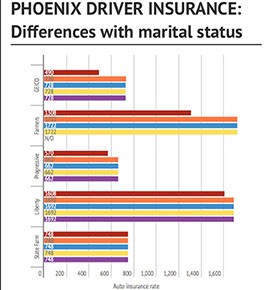

The report found differences between customers based on their marital status could be large: In Phoenix, for example, rates were sometimes as much as $400 a year higher for a widow than a married woman.

Four of the five insurance companies cited in Phoenix – GEICO, Farmers, Progressive and Liberty – had lower rates for the hypothetical married customer. Rates at State Farm did not vary with marital status, the report said.

Calls to the individual companies were referred to the Insurance Information Institute, where Michael Barry said it is not surprising to see different rates for different people.

“The auto insurance industry has generally found that married drivers pose less of a risk to insurers than single ones,” said Barry, adding that it is a “consensus opinion that has emerged over a period of decades.”

Not all risk factors are based on driving records, Barry said, noting that insurers in some states look to credit scores because they “have found that people who handle their finances correctly are less likely to file claims.”

Hunter disagreed with the notion that rates should be influenced by anything besides your behavior behind the wheel, but he said “credit score has more impact than anything else” on rates, even more so than drunken driving incidents most times.

Other advocates agree with Hunter, arguing there should be no correlation between auto insurance risk and socioeconomic factors.

“What does paying your credit card on time have to do with your driving?” asked Ed Mierzwinski, consumer program director for the Arizona Public Interest Research Group.

“As far as I know, insurance companies are using a variety of unfair rating tools,” Mierzwinski said.

“Instead of using legitimate factors, based on causation,” Mierzwinski said the federation’s study points out “insurance companies trying to maximize their profits.”

Basing rates, at any level, on socioeconomic factors “undermines the safety” that auto insurance rates were once founded on, Hunter said. He said there is “more and more use of factors that have nothing to do with driving.”

But Carlson said that when underwriters determine premiums, “It all comes down to risk assessment.”

Companies compile all kinds of information, from marital status to driving records, he said, that helps them “determine what sort of risk they want to take with a particular customer.”

“They may target you, they may target me,” Carlson said. But ultimately they will “come up with a rate they think we will accept, so they can try to secure business.”

“They might think single people have an increased risk for that company,” he said of the federation report findings.

Hunter said the report also clearly shows “a widow penalty,” as insurance rates increase for a woman whose husband just died. The practice “just about takes the cake,” he said.

CFA Executive Director Stephen Brobeck said raising rates in instances like that “seems inhumane.”

“It’s not at all clear” why companies use such factors, he said.

^__=

Web Links:

_ CFA report: http://www.consumerfed.org/news/1106

_ Consumer Federation of America: http://www.consumerfed.org/

_ Insurance Information Institute: http://www.iii.org/

_ Arizona Department of Insurance: https://insurance.az.gov/

_ Arizona PIRG: http://www.arizonapirg.org/

^__=

SIDEBAR:

SF ISO insurance

The Consumer Federation of America sought car insurance quotes for a hypothetical customer in 10 large cities, changing her marital status but keeping all other factors the same. The hypothetical driver was:

– 30 years old

– Female

– Driving since 16

– No accidents or moving violations

– High school degree

– Bank teller

– Renter in ZIP code with $30,000 median household income

– Driver and owner of a 2005 Honda Civic

– Has insurance purchased three years ago

^__=

The Consumer Federation of America study sought quotes from different insurers in Phoenix and found most charged less to married drivers. Click above for an interactive chart. (Chart by Aubrey Rumore)

A Consumer Federation of America study of auto insurance rates in 10 large cities showed married drivers were generally charged less than nonmarried drivers. (Photo by Light Stalker via flickr/Creative Commons)